Portfolio and thesis update #1

Portfolio and thesis update #1

A quick overview of my 4 most significant holdings thesis

As you may know, I run a very concentrated portfolio. One month, I might outperform the S&P 500; the next, I might be back at zero. That is why I don’t really care about performance in a single year and, especially, a single quarter.

Let me remind you of my strategy:

Buy wonderful companies that have clear catalysts to rise in the coming years;

Track record and predictability decide the weighing;

I want to be lazy, meaning I always prioritize adding to existing positions over getting new ones if the new stocks do not increase the average company quality of the portfolio.

I treat businesses like they were my family’s business. Would I be comfortable having this company as 100% of my net worth and being unable to sell for at least 20 years? If the answer is yes, I look further.

Now, let’s discuss the companies I own and the reasons behind them.

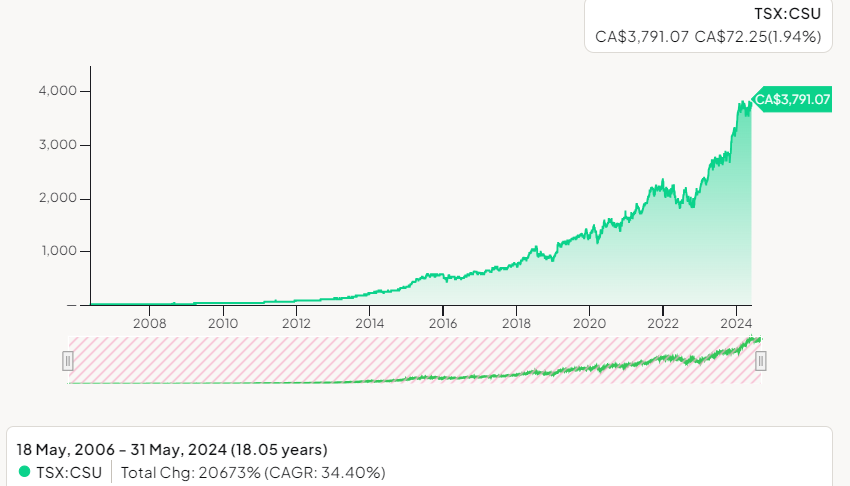

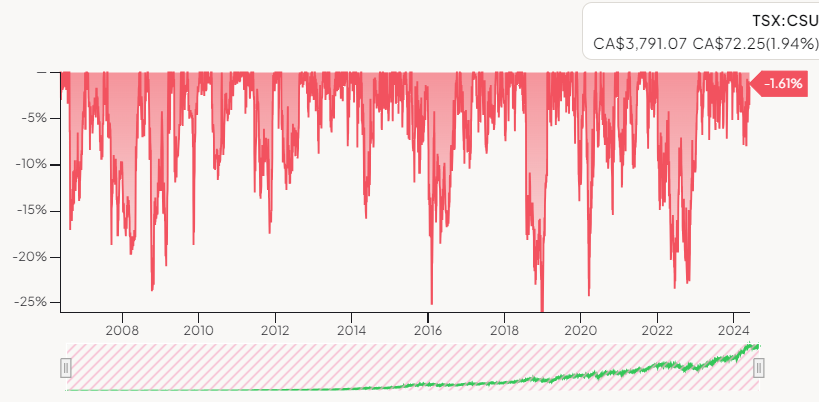

1. Constellation Software (32%)

Overview:

Ticker: CSU 0.00%↑

10 Yr. revenue growth: 20.68% CAGR

10 Yr. EPS growth: 20.04% CAGR

2 Yr fw. revenue growth: 20.51%

2 Yr. fw. EPS growth: 54.46%

ROE: 38.56%

ROCE: 29.9%

ROIC: 9.57%

Yes, you read that right. A third of my equities portfolio (and 25% of my net worth) is in Constellation Software. Why?

It has not only proved to be a high-growth compounder but also a resilient market-leading company in significant downturns.

This performance and sturdiness are not a coincidence. Constellation Software owns more than 700 companies in over 100 different markets worldwide. It’s strategy? Buying niche vertical software businesses with high margins and domination in the specific industry.

Even though scaling has become a slight problem, CSU has shown an exceptional ability to adapt and overcome this hurdle.

Valuation

Trailing P/E: 102.7

Forward P/E: 32.8

Forward P/FCF: 24.3 (more than 4% yield!)

Thesis for outperformance

This is probably the only company where I am not too worried about where it goes from here. That is the result of having complete trust in the company’s mystified genius capital allocator and CEO - Mark Leonard. CSU doesn’t need a catalyst because they ARE their catalyst. Continued growth and quality acquisitions will be more than enough to provide constant outperformance and stability in my portfolio.

To end Constellation talk, I will quote my mentor’s answer to my question about trimming CSU: “You could trim some profits, but in 2-3 years, I suspect you will hit your head on the wall if you check the price.“

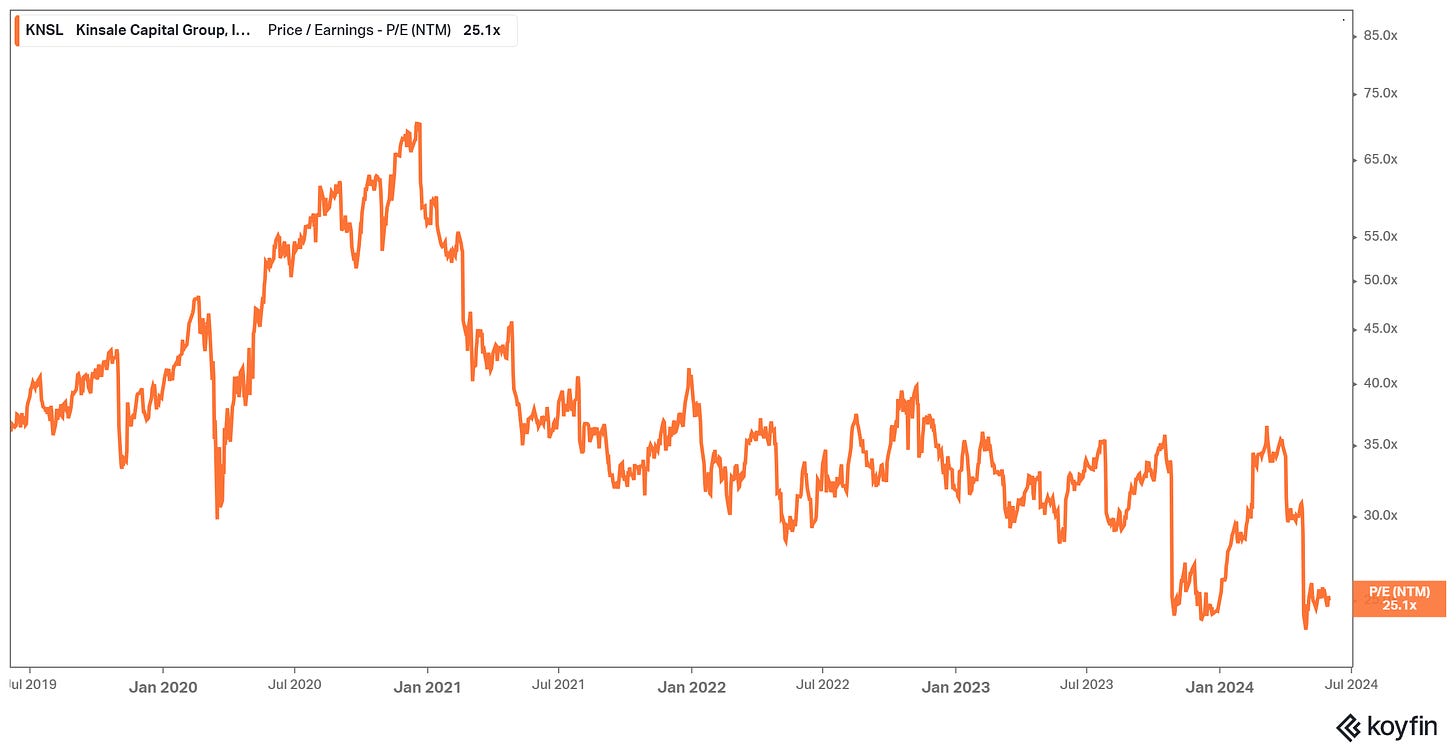

2. Kinsale Capital Group (18.41%)

Overview:

Ticker: KNSL 0.00%↑

5 Yr. revenue growth: 40.44% CAGR

5 Yr. EPS growth: 48.57% CAGR

2 Yr fw. revenue growth: 23.78%

2 Yr. fw. EPS growth: 15%

ROE: 23%

ROCE: 25.42%

ROIC: 7.38% (not the right metric to judge KNSL’s performance, tbh)

Kinsale Capital Group is a specialty property/casualty insurance company that provides E&S (excess&surplus) insurance products in the United States. It markets and sells them in all 50 states. Through its extensive and market-leading processes, Kinsale manages to shift the “High risk - high reward“ balance in its favour.

This is another big part of my net worth that only increased after Kinsale experienced a 30%+ drop in recent months due to worsening market expectations and a weakened outlook.

I won’t write much in this post because you can find my recent detailed deep dive here, but to sum it up, it is one of the most efficient, profitable, and fast-growing insurance companies that continues to outperform the market.

Valuation

Trailing P/E: 25.7

Forward P/E: 25

Thesis for outperformance

I believe that KNSL 0.00%↑ is currently pretty attractively priced at almost 25 forward P/E, compared to a median of 38 with a still relatively high projected growth.

I expect the efficiency to continue and for Kinsale to remain the growth leader even in a worse market, and continue taking market share, significantly increasing from the <2% it has today.

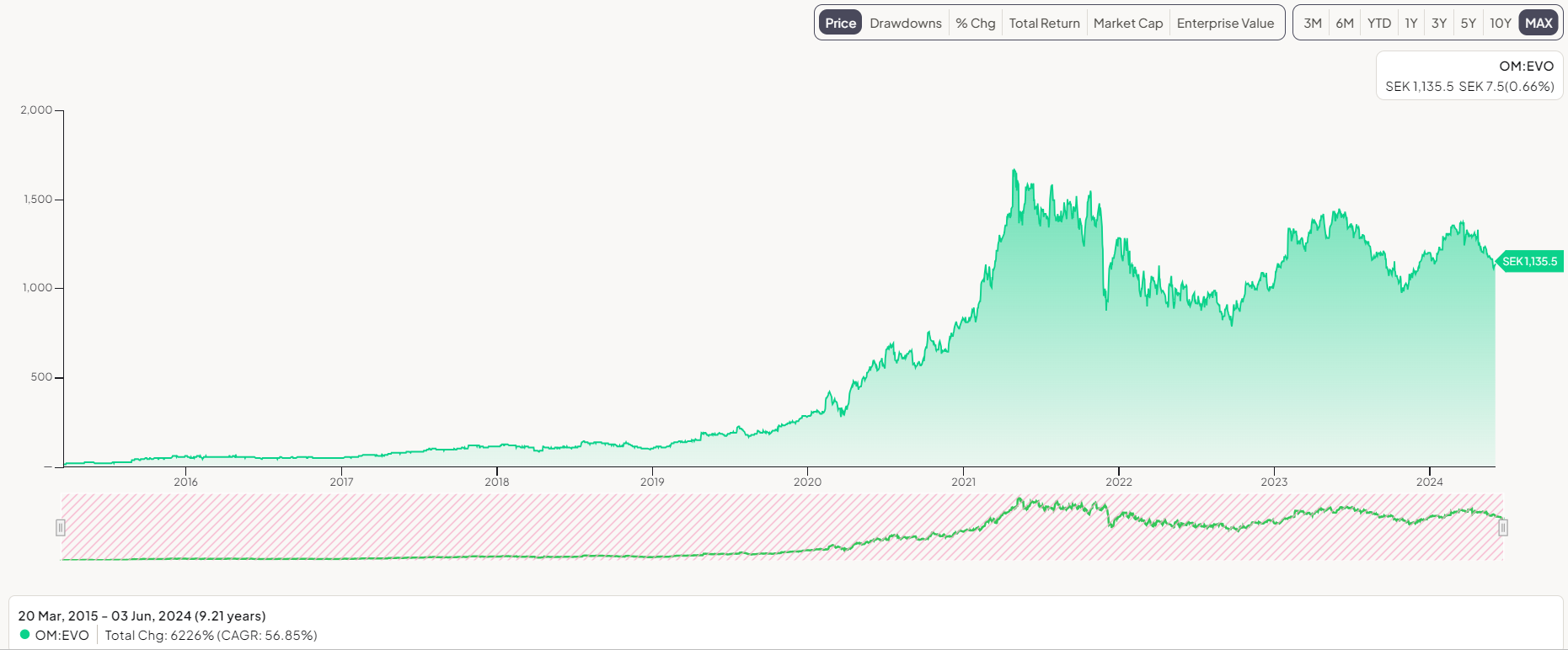

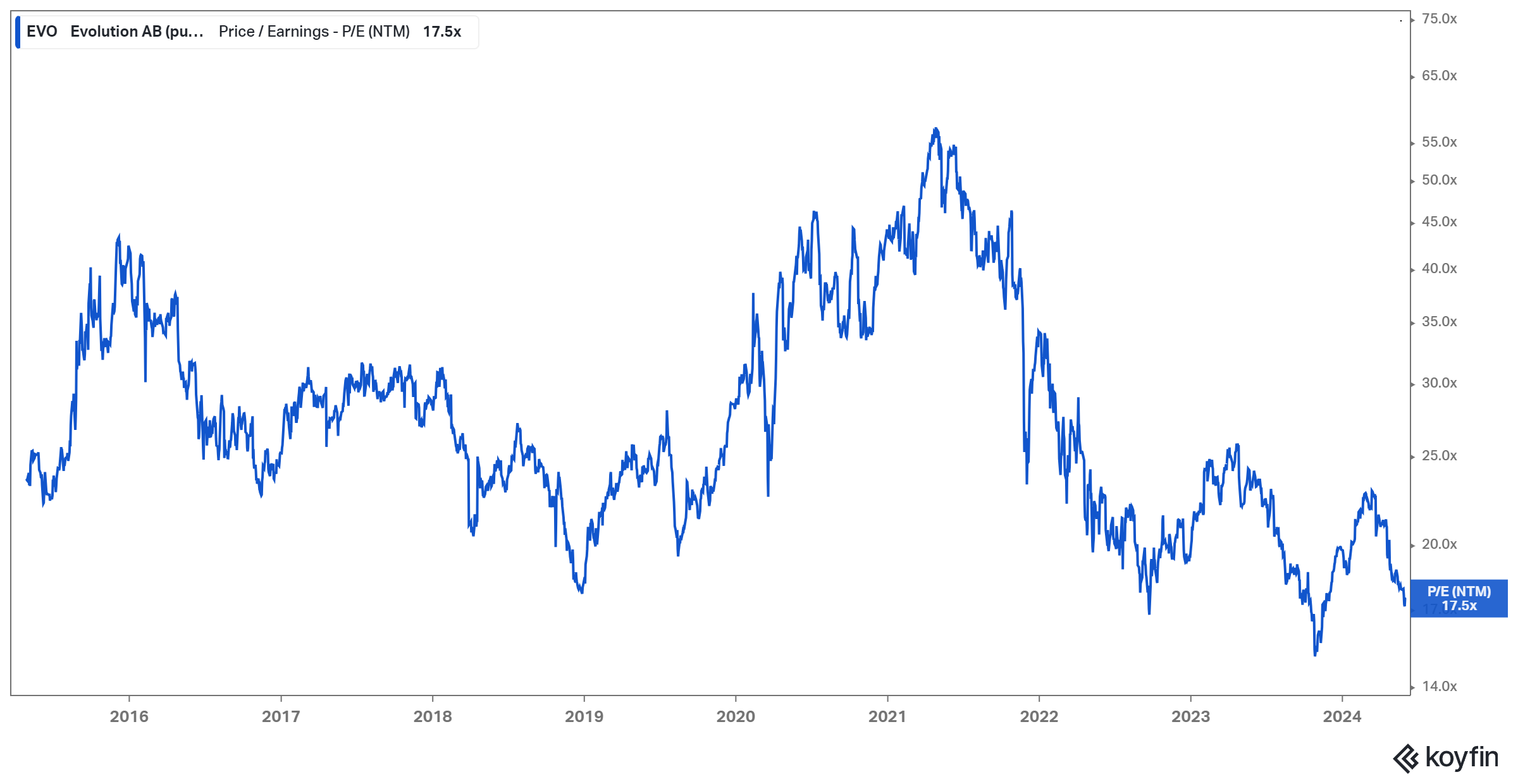

3. Evolution AB (12.6%)

Overview

Ticker: $EVO.ST

5 Yr. revenue growth: 46.9% CAGR

5 Yr. EPS growth: 56.9% CAGR

2 Yr fw. revenue growth: 17.1% CAGR

2 Yr. fw. EPS growth: 13.1% CAGR

ROE: 39.75%

ROCE: 39.17%

ROIC: 42.27%

Net margin (just had to include this :D): 58.2%🤯

Evolution AB is a Swedish company that develops, produces, markets, and licenses online casino systems to gaming operators in Europe, Asia, North America, Latin America, and internationally.

Many people criticize me for holding this “sin“ stock and risking so much in a company with regulatory risks. The way I think about it, though, is that Evolution provides entertainment, and people pay for having fun. I believe this is a fair trade-off, and most people will never see it as investing of sorts.

Now, let’s get to the investment part.

The stock was on a tear a couple of years ago, and even though the company has been steadily increasing all of its metrics, it has just been playing catch-up to the huge price move we saw. In my opinion, this consolidation serves as a great position-building point at a very attractive valuation and growth prospects.

Valuation

Trailing P/E: 19.5

Forward P/E: 17.4

Forward P/FCF: 17.5

Thesis for outperformance

Evolution is a master of efficiency and profitability, consistently growing at all times with very low CAPEX requirements. I believe that this consolidation is nearing an end, and multiples should start following growth soon. As business and its fundamentals grow, I have no reason to worry.

If you want to read a great Evolution overview, I recommend Fundasy’s write-up here.

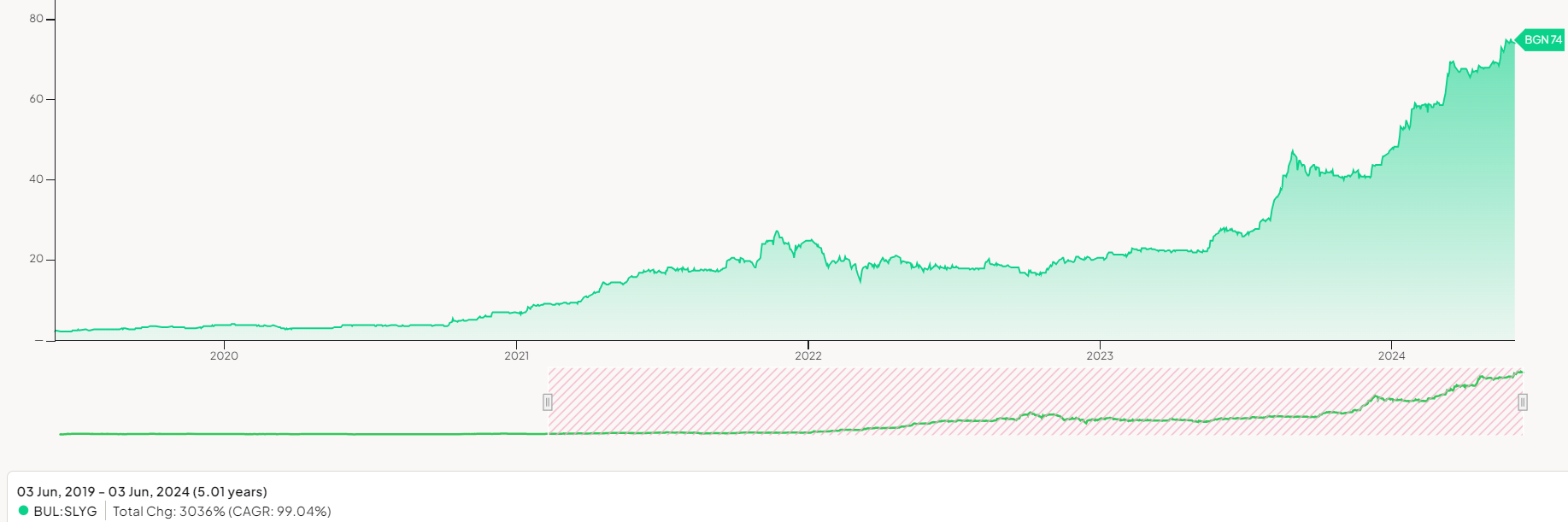

4. Shelly Group (11.35%)

Overview

Ticker: SLYG 0.00%↑

5 Yr. revenue growth: 27.59% CAGR

5 Yr. EPS growth: 48.06% CAGR

2 Yr fw. revenue growth: 41.6% CAGR

2 Yr. fw. EPS growth: 34.7% CAGR

ROE: 27.5%

ROCE: 27.1%

ROIC: 33.2%

Shelly Group is a Bulgarian company that designs, manufactures, and distributes IoT (Internet of Things) products in Europe and the United States. It is probably my highest conviction, though risky, investment. If the past and future growth of EPS didn’t pique your interest, Shelly has returned over 30 times over the past 5 years.

The company has exceptional management, growth, and profitability metrics. I believe it is fairly valued for the quality it provides.

Shelly started as a telecommunications business that evolved into tech, IoT, and now - the cloud. The fast iteration shown by the management makes me confident that the company will be able to face any hurdle that comes its way in this fast-changing industry.

Valuation

Trailing P/E: 37

Forward P/E: 29

Forward P/FCF: 639 (doesn’t say much as they reinvested everything, got more inventory, manufacturing space, etc.)

Thesis for outperformance

Shelly is probably the highest-growing company in my portfolio. It is currently continuing its expansion into Europe, pumping out products like never before, and executing in a very efficient and profitable way. I expect to get at least 20%, if not more, annual returns for the next five years.

You can check out a full deep dive I wrote on Shelly here.

That’s it for today. I will reveal the other half of my positions (plus a new buy!) next week for the free subscribers, but if you want to get it today, you can subscribe to the paid version.

Both ways, I am grateful to have you as a reader and am committed to staying free to read for at least one year.