Potential 10x? Shelly Group uncovered 🇧🇬

Potential 10x? Shelly Group uncovered 🇧🇬

An overview of a high-growing Bulgarian small cap trying to achieve world domination in the smart home industry.

Shelly group found its way into my watchlist after another screen of potential high-quality, high-growth companies in Europe. Seeing it rise for many weeks, I finally decided to briefly check out the company; I saw something spectacular—extraordinary growth, amazing efficiency, and an even bigger stock run-up over the past five years. In this deep dive, I hope to showcase why I believe this could be a worthy addition to your portfolio.

Overview

Ticker: SLYG.F (original listing in Bulgaria)

Market cap: 635M Eur

Price: 35 Eur

Year founded: 2003 (IPO- 2016)

Founder/CEO: Dimitar Dimitrov

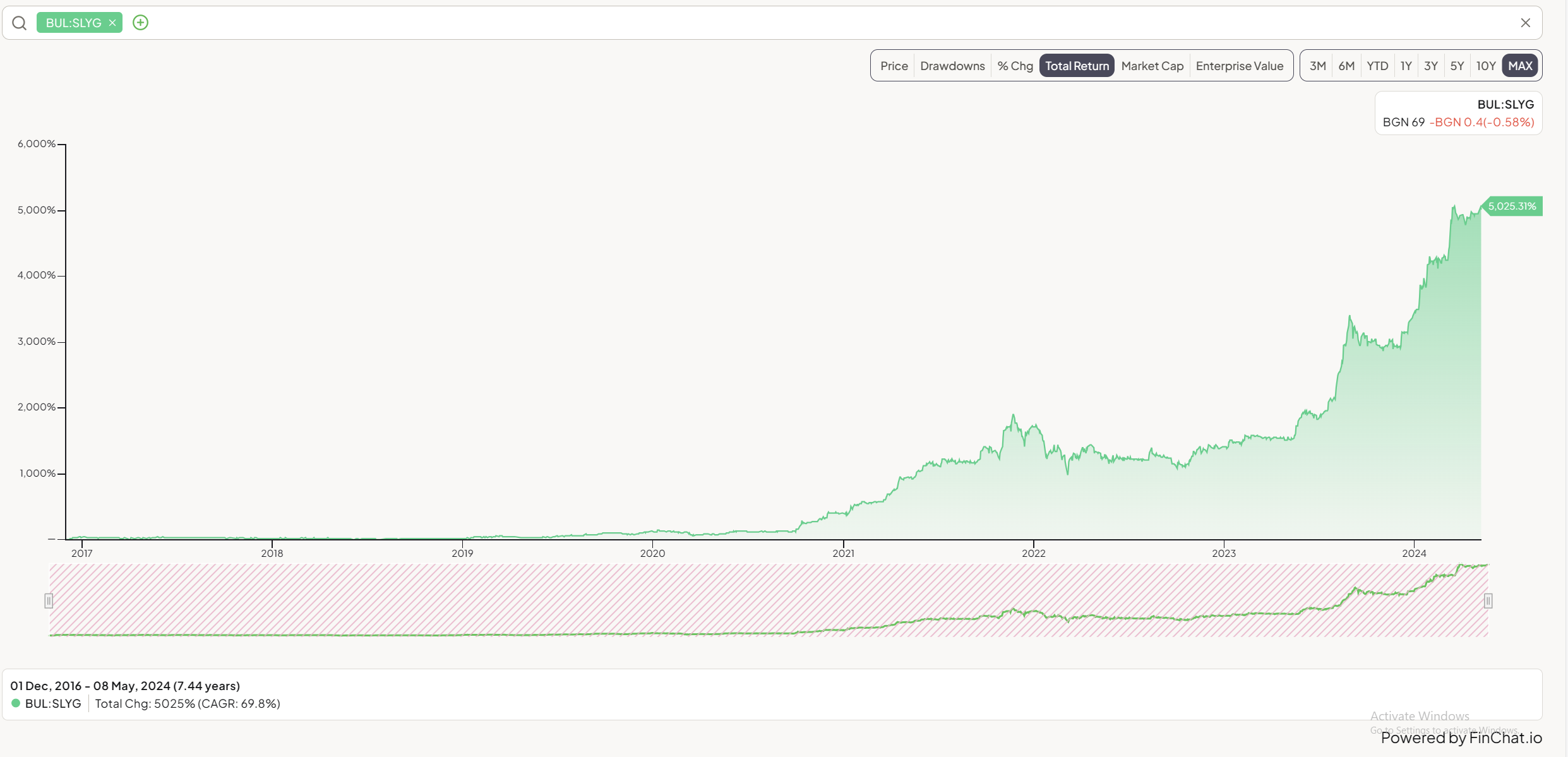

CAGR since IPO: 69.8% (5Yr CAGR - 109%)

Shelly Group is a Bulgarian company that designs, manufactures, and distributes IoT (Internet of Things) products in Europe and the United States. The company offers smart home devices that help save energy and also a branch of products that monitor children, pets, and automobiles. Additionally, they have launched a cloud platform that can connect all smart home devices to create a coherent system of gadgets.

Product

New product launches are one of Shelly Group’s biggest and most significant growth drivers. In 2023, Shelly launched 21 new products and now has over 70 in total. Now, hear this: in 2024, they have already launched 15 new products and are planning to launch/update an additional 25-45 this year.

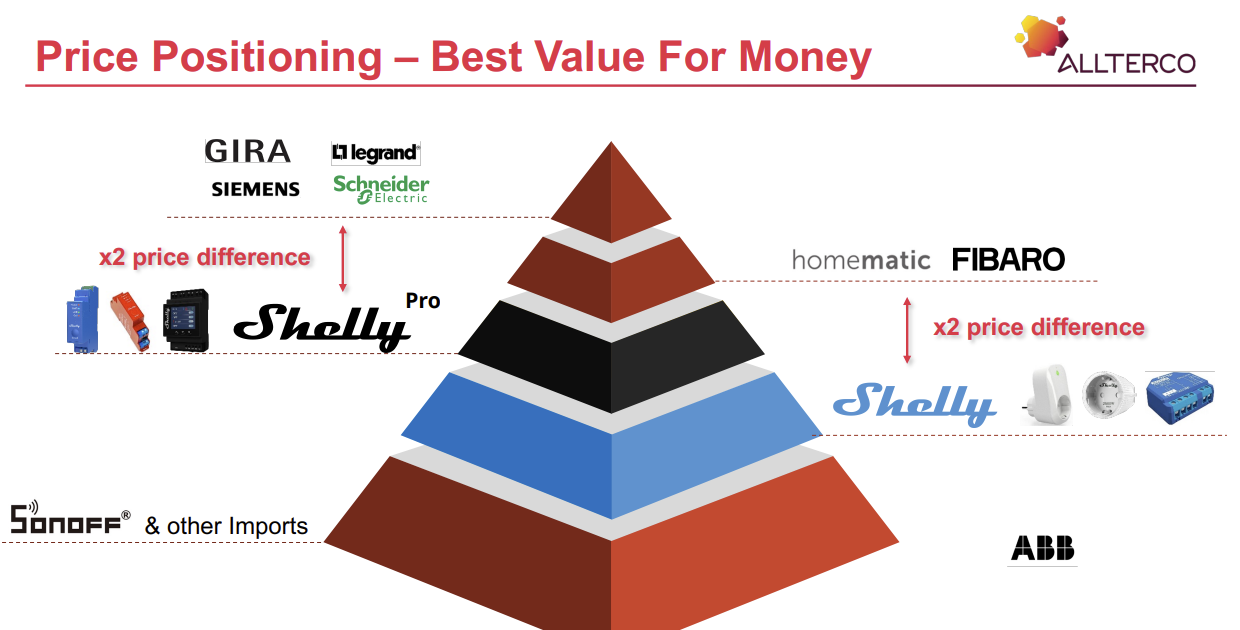

Shelly’s products are around 50% cheaper and very easy to install compared to their competition, initially attracting more price-conscious DYI customers. However, I believe this is only a minuscule part of what Shelly could be.

Cost example: I searched up a basic “Schneider” (one of the biggest competitors) smart relay that is similar to Shelly’s and this is what I found:

Vs most expensive Shelly Product I found (you can obviously spot that the configuration is more simple which is why it’s cheaper but that’s what beginners need!):

I also managed to find cheaper alternatives like Bosch smart relay but it is worse than the normal Shelly relay and still 2x more expensive.

These are the segments that Shelly mainly operates in:

Home Efficiency

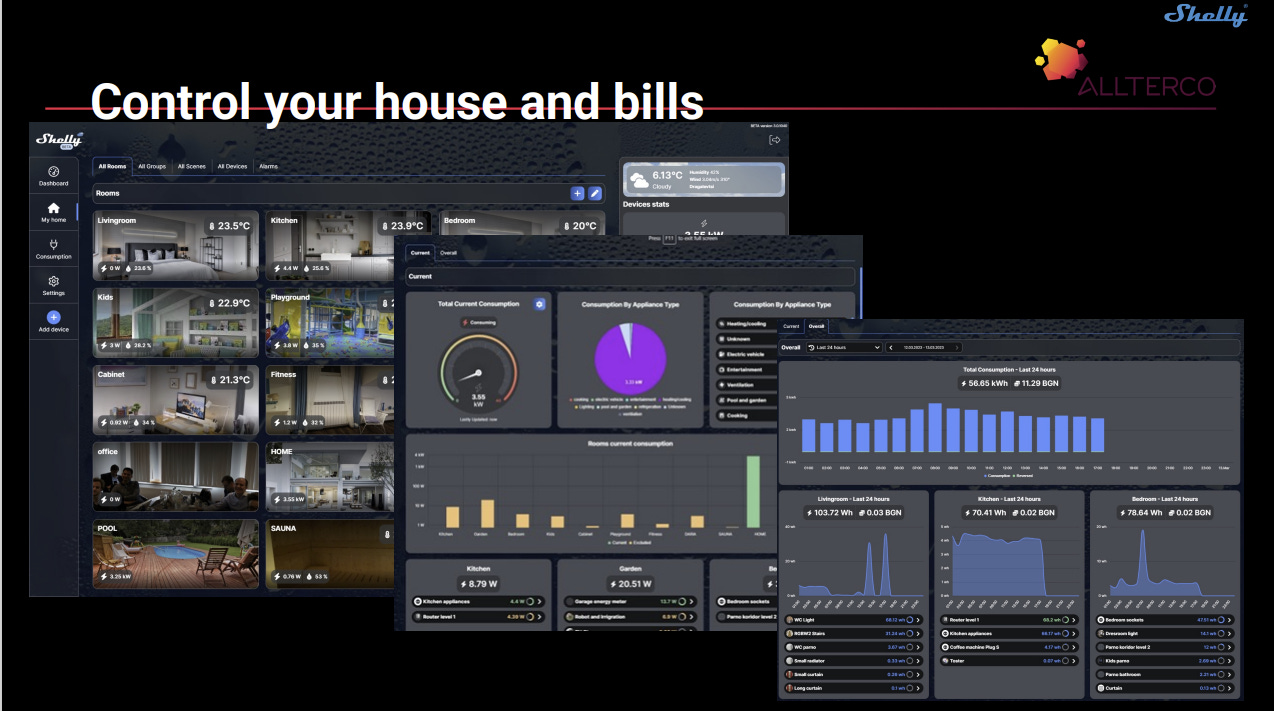

This is probably the company's most important product group. They manufacture smart relays, shown below, which monitor the energy you consume in your house and feed data to the app mentioned below to show visualizations of the results. This allows you to see where you consume the most energy, and how you can optimise your electricity spend. I will talk about this later, but the main point is that as Europe becomes increasingly climate-conscious, new laws are being passed that require houses to be more energy-efficient. This is where Shelly can come in and help save money at a relatively low cost.

Source: 2023 Q3 presentation Smart-home

The same devices that can help you track and optimize your consumption can be used for house automation (even when the internet is down) - shutters, roll-outs, lights, garage doors, climate, etc. For example: “Increase temperature to 23 degrees Celsius when outside temperature hits X” or “Open shutters when the clock hits 8 a.m” etc.

One of the most interesting things about Shelly Group is its philosophy of making everything as open as possible. Their products are completely programmable, so it makes sense that their current clients are mostly DYI people who enjoy doing things themselves. More about that later on.

Cloud service

Shelly Group has built a monthly fee (first recurring revenues) cloud service that allows it to connect all its products into one app and create detailed visualizations with data from each one. The app's user base has grown significantly by 573K last year and now has 1.25M users in total.

The app has a free basic version and a premium one that costs 4 euros a month, which is not too much, so the price-oriented Shelly's customers would not use it, but also enough so the company can get a real margin boost from the product. The revenue from this segment is still insignificant but I believe that with time, it will scale enough so to provide a meaningful contribution (especially as they increase prices).

From 2022Q4 report

You can watch this video to understand Shelly’s relays a bit deeper or visit shellyuniversity.com to learn about what is even possible with Shelly’s products:

History

Shelly Group (initially Telacomm and then Allterco) was founded as a telecommunications business in 2003 by the still-running CEO Dimitar Dimitrov.

In 2013, management decided to venture into the IoT business by developing the first smart home system. In hindsight, it was an excellent move for them as the segment grew much more rapidly than their telecom business. Eventually, the old operations were divested in 2019 to focus on the Shelly brand.

Shelly Group was listed on the Bulgarian Stock Exchange in 2016, the Frankfurt Stock Exchange in 2021, and finally, in 2024 - XETRA. This shows a continuous focus on improving stock liquidity and recognition. Since the first listing, the stock has risen 50x!

The Industry

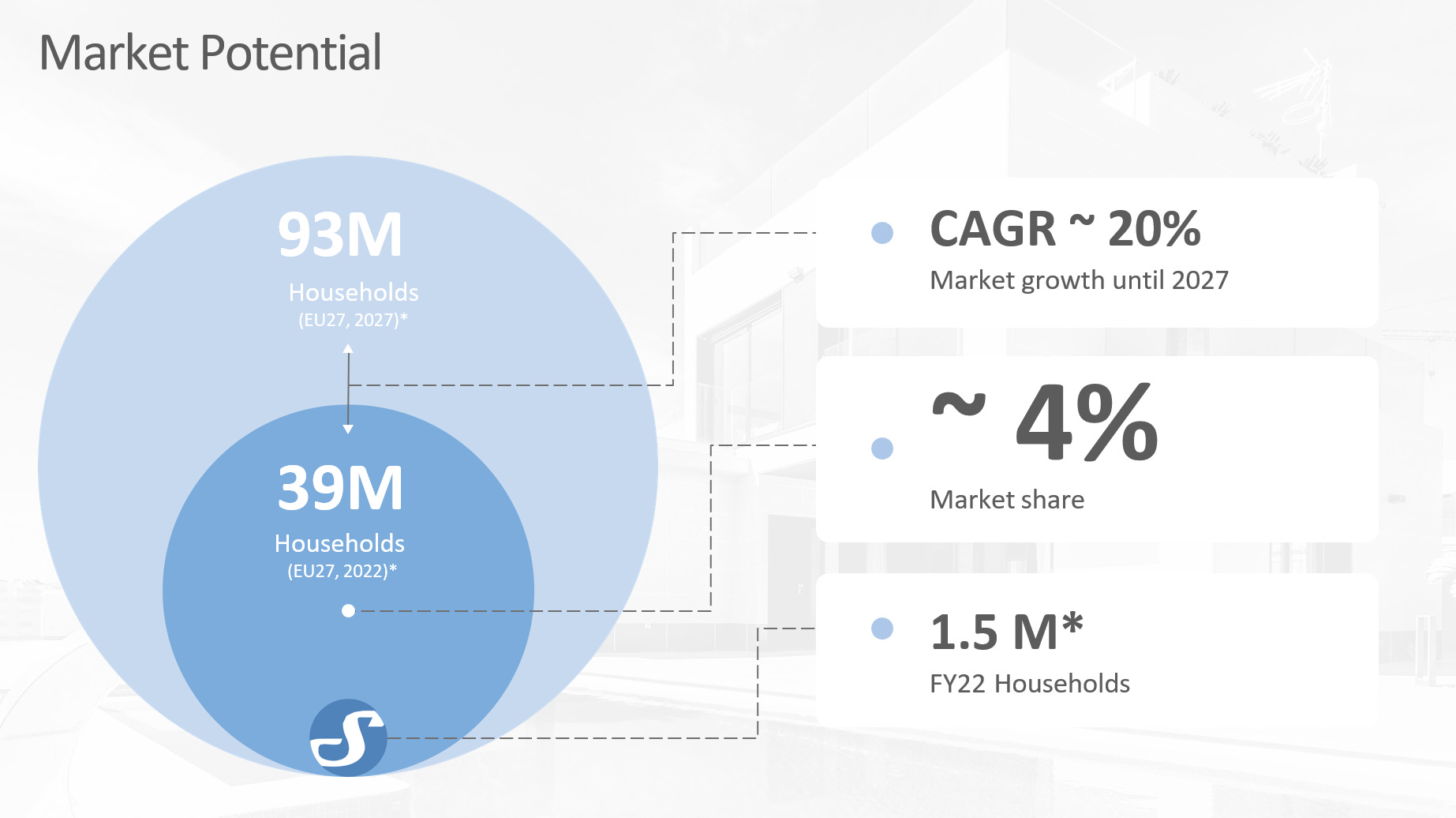

The worldwide smart home market is projected to grow by 12.3% annually until 2032, and the IoT - 15-20%.

Even though this rate alone is outstanding, Shelly Group has grown at triple this speed. I expect the outperformance to continue as it rolls out more products and expands worldwide.

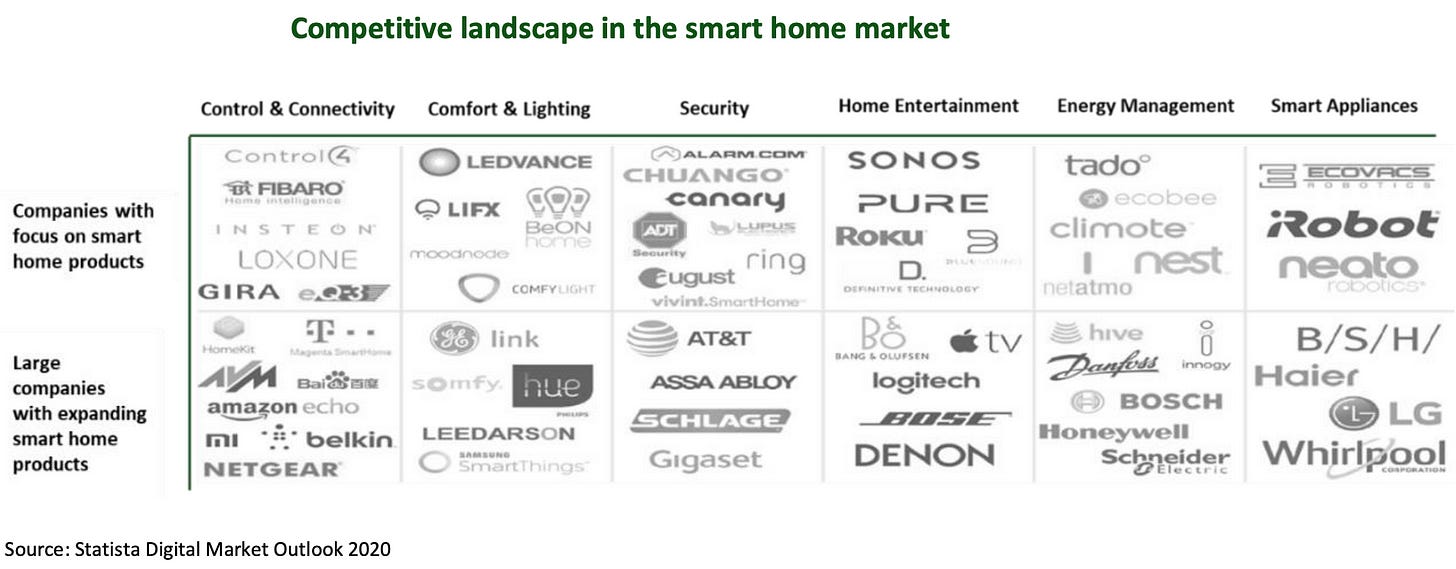

The market is dominated by brands like Google, Amazon, and Siemens, but Shelly Group has managed to stay competitive by focusing on more niche products rather than the most sexy ones.

If you are wondering whether the potential market is big enough, you can relax because every single home in the world would benefit from Shelly’s products. The question is whether they will want to.

Regulatory push to make homes more efficient

More than 2/3 of European houses are not energy efficient and require efficiency tracking. The European Union is already releasing more and more regulations regarding target efficiency for individual homes, and this is where Shelly Group can come in to save the day/become a target budget product.

How does Shelly Group stack up in this highly competitive market?

Management

One of the things I love most about about Shelly is its management team, so let’s start with that.

Group CEO and founder Dimitar Dimitrov, together with Svetlin Todorov (co-founder and head of USA operations), own more than 64% of the company.

The good thing is that their interests are obviously very much aligned with the shareholders, but on the other hand, it reduces liquidity. Management has hinted that, if needed, they would sell a very small stake but only as a last resort - a very good sign for the shareholders that the executives have this much conviction in the company.

Interestingly, a third person—Wolfgang Kirsch—joined the Shelly Group in 2021. Previously, he managed the expansion of a leading European consumer electronics brand, which shows that he has the experience needed to make Shelly a REAL global company.

He is listed as a co-CEO and has been crucial in Shelly's expansion to Europe, now its fastest-growing and biggest market. Unfortunately, he doesn’t hold that many shares in the company, but I hope that with time, he will be able to build up a position.

My takeaways about the team:

Fast iteration.

During chip shortages, the team quickly modified its products to fit other chips too, which led to continued normal operations. Afterward, they released their own chip so that this problem would never happen again (+ to improve the product performance).

Forward-thinking

After going through quarterly calls, I noticed one thing—they always provide solutions and address problems that might arise in the future. For example, they have already talked about how they plan to move production to Vietnam and use their acquired company's factory in Italy in case political tensions with China worsen and they cannot continue their production there. This is crucial in this super fast-changing industry.

Careful and disciplined capital allocation

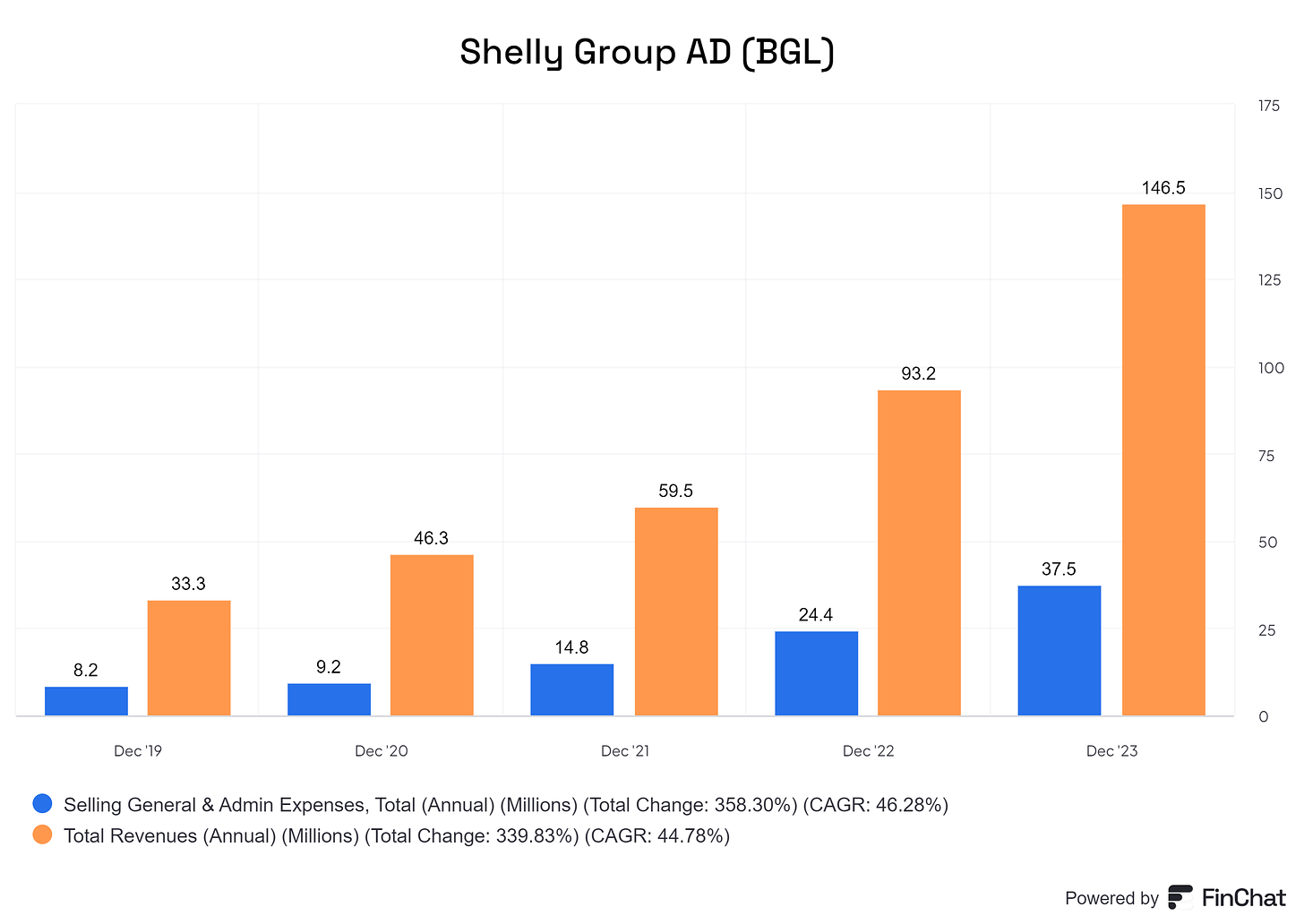

To date, we have seen normal (not great, but ok) dilution and very careful capital allocation. Shelly has almost no debt and has been expanding through word-of-mouth without spending a fortune on marketing (marketing expenses are only 4.5% of revenue). Other selling expenses are also fine (same SG&A margin as Amazon has now while being at a much lower scale and growing at very high double digits). High expense increases are due to new sales teams implemented in all of Europe. This is an investment that will show reaped results in years to come.

Overdelivering

A typical “problem” with this company is that they always have to raise their targets because they usually achieve estimates way earlier than anticipated. The CEOs speak very straightforwardly, don’t try to overhype or underplay the company's trajectory, and seem knowledgeable. I would highly recommend watching some quarterly calls.

It has also been mentioned by the CEO that even though they put out already pretty high estimates for the market, the internal targets (and bonuses based on them) are even higher.

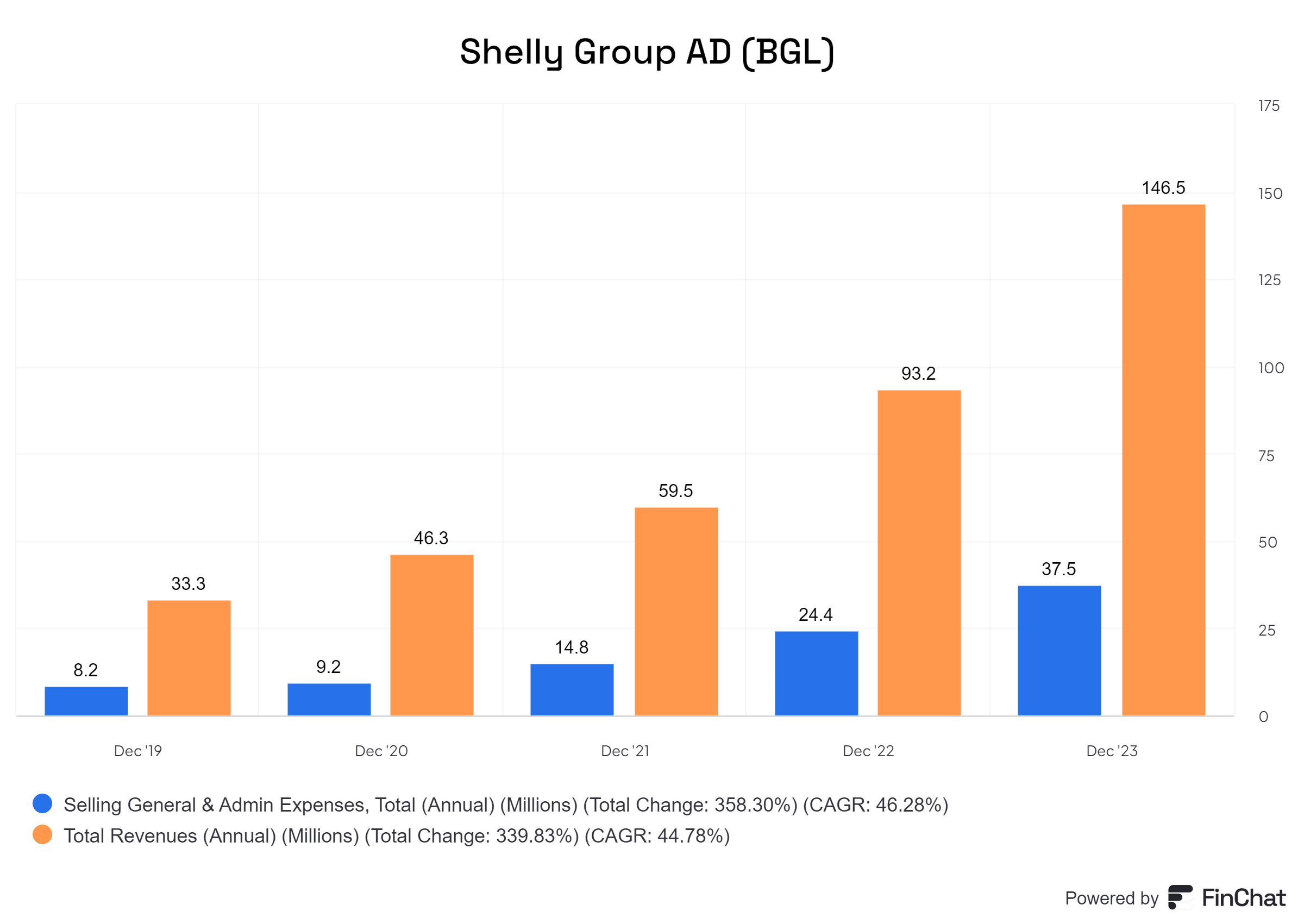

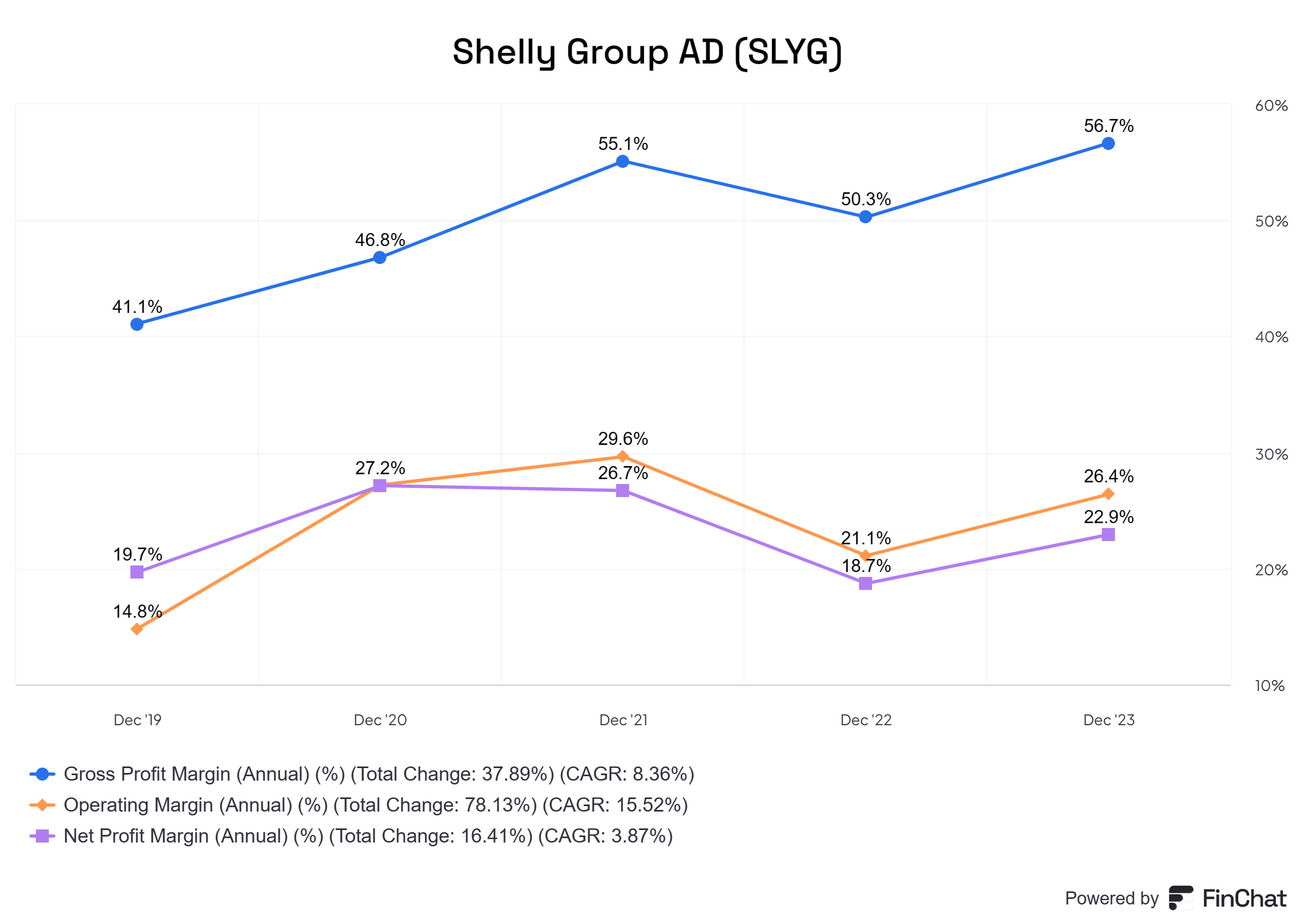

Financials/metrics

Shelly Group is not only a fast grower but also a very efficient company. This is reflected in their financials:

Margins:

Gross margin: 57%

Operating margin: 26.4%

Net margin: 23%

They manage to keep margins high even by having prices that are 50% lower than the competition!

Efficiency (5Yr Avg):

ROA: 22% ✔️

ROE: 26.5% ✔️

ROIC: 31.4% ✔️

Balance sheet:

Total assets: 128M BGN (66M Eur)

Total liabilities: 18M BGN (9.51M Eur)

Current assets: 108.5M BGN (55.5M Eur)

Current liabilities: 16.4M BGN (8.4M Eur)

Interest coverage ratio: 168 ✔️

As mentioned before, the management is really careful with the company’s capital. Even though this provides much-needed protection against downturns, I would like to see them start taking on at least a little debt to fuel more growth in the future.

Anyhow, the company is in great financial shape, and I believe this adds a real buffer against the risks mentioned below.

Opportunities

Very active product pipeline

As mentioned, Shelly Group continues to pump out products at an unbelievable pace, further increasing their product selection and fueling revenue growth. This year, they are expected to increase their number of products by 50%! This will bring their total count to over 100, which will help take market share from the competition.

Shelly has also developed its own Shelly chip and operating system, which increases the power and variety of functions.

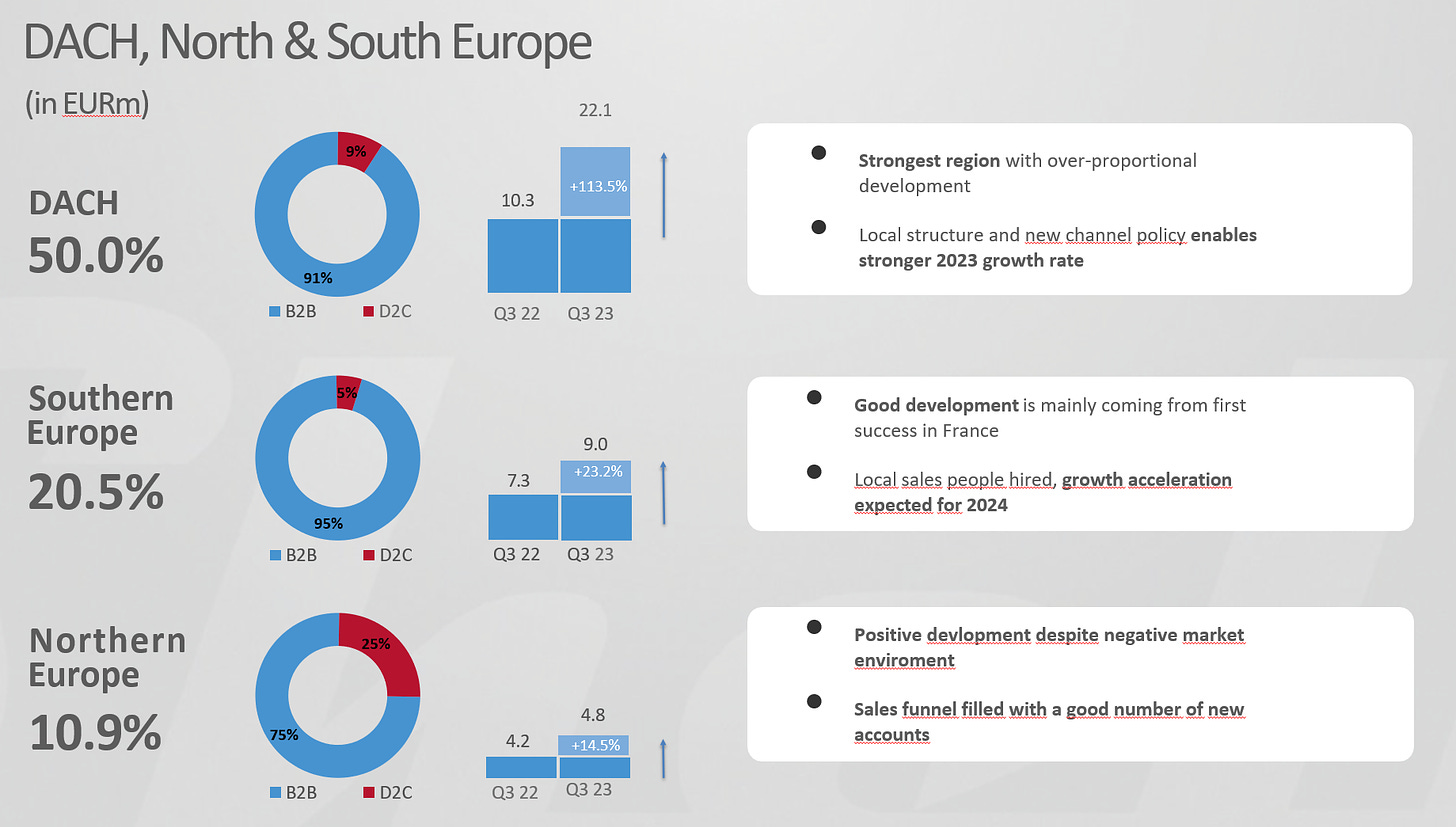

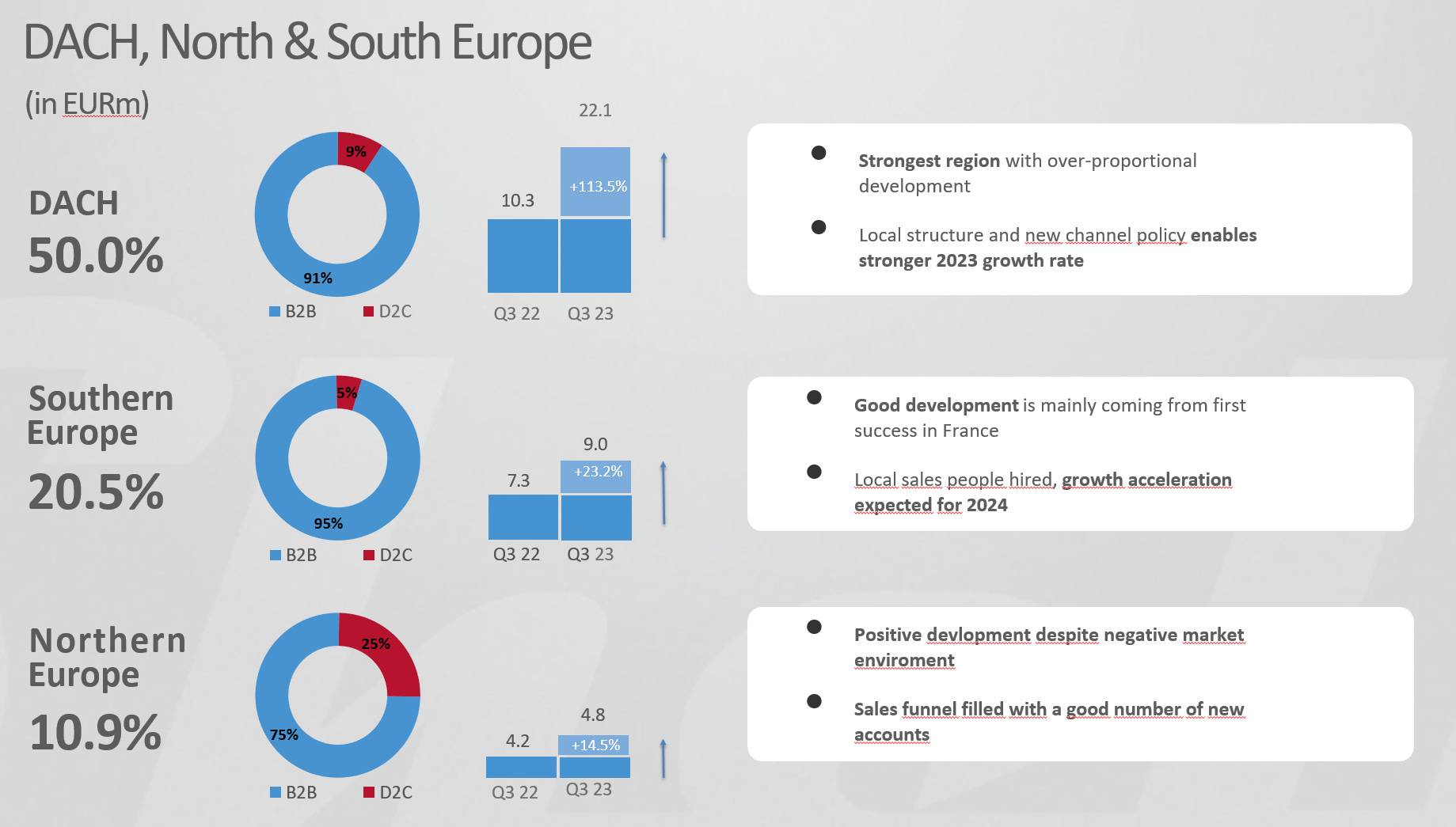

Continued Europe expansion

The company has started deploying individual sales teams in more EU countries, such as Italy, Poland, Turkey, and the Benelux region. Since they have already successfully expanded into Germany, I believe the same should be achievable in other countries.

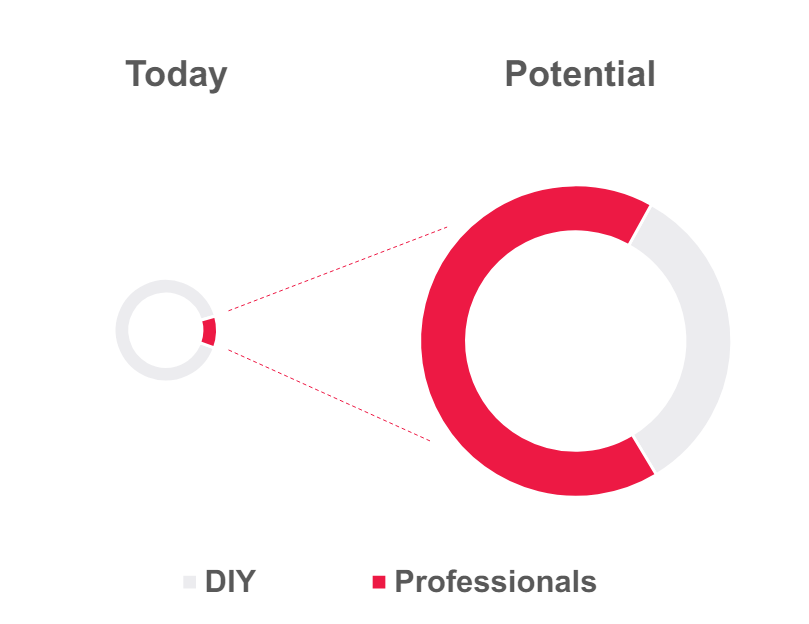

Source: 2023 Q3 report Professional installers market push

So far, most of Shelly Group’s customers are DYI aficionados who love programming their gadgets and functionality themselves. This leaves a vast untapped market for the company as professional installers could simultaneously make Shelly products the default choice for thousands of homes.

To achieve this, it has already signed the first contracts for professional installers distribution in 2024 and has trained over 3000 professionals in the hope that they will choose Shelly Group as their preferred brand.

Source: quarterly report Marketing spend increase

As I’ve noted, Shelly Group spends almost no money on marketing, and all of its sales so far have been driven by DYI and other communities, word of mouth, and Amazon recommendations. As these sources of growth get saturated, Shelly could start increasing their marketing spend, continuing the growth trajectory.

Strengths

Driven management aligned with the shareholders

From all the quarterly calls I've listened to, it is clear that management is driven to deliver shareholder value. Their 60%+ insider holding makes me very confident that, in the long term, they will do their best to not only safeguard the company but also substantially increase its value.

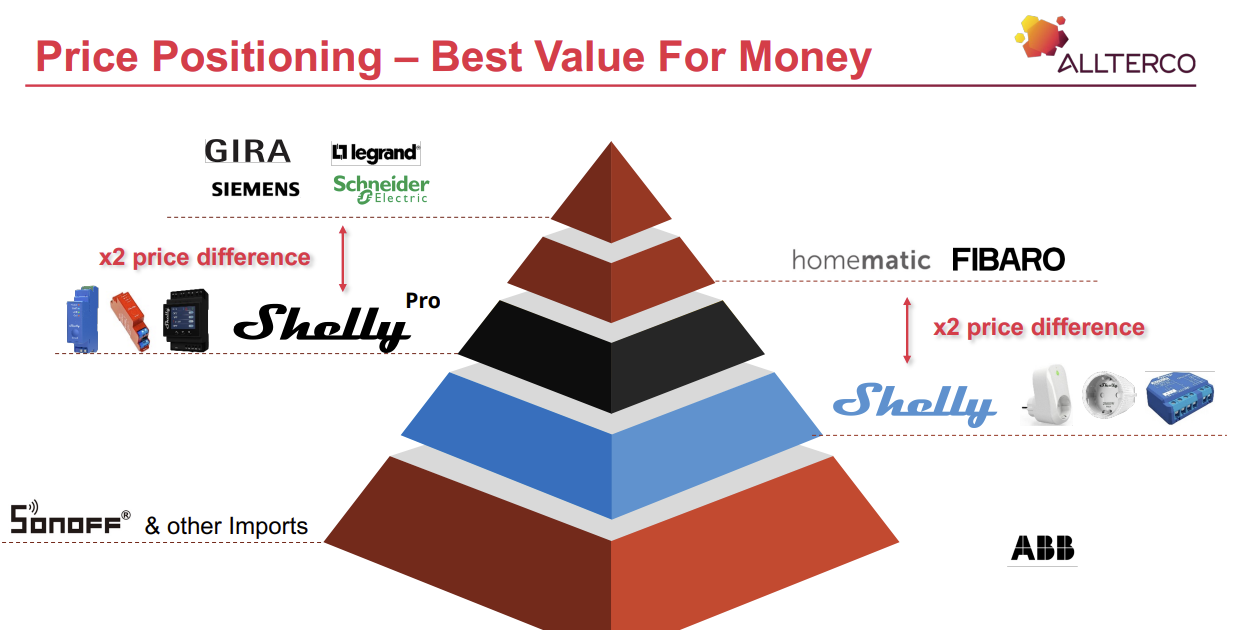

Product quality-cost ratio

Shelly Group has mentioned that most of its products are priced around 50% below their competition, even while maintaining decent quality. This means they are and will continue to take market share from the competition. The company's products are also among the easiest to use, making them the best choice for newcomer buyers.

Source: 2022 Q4 presentation Robust balance sheet, margins, and overall financials

The financial strength of Shelly Group is, in my opinion, excellent and will continue to be so as the management is scrupulous with taking on debt and additional expenses.

Programmable, open products

Many companies fear making their products 100% compatible with other brands because they believe this could reduce their own brand sales. Shelly Group is open to all programming and compatibility with other brands. This creates a competitive advantage that further steals market share from the competition.

Source: 2022 Q4 report High customer satisfaction

Most of the company’s products have 4-5 star reviews on Amazon. This is important as newcomers come to Amazon to search for their first products to retrofit their homes. As they buy the higher-rated Shelly products, it is likely they will stick with the same brand for ultimate comfort and, in the end - become lifelong customers who buy more products that Shelly releases.

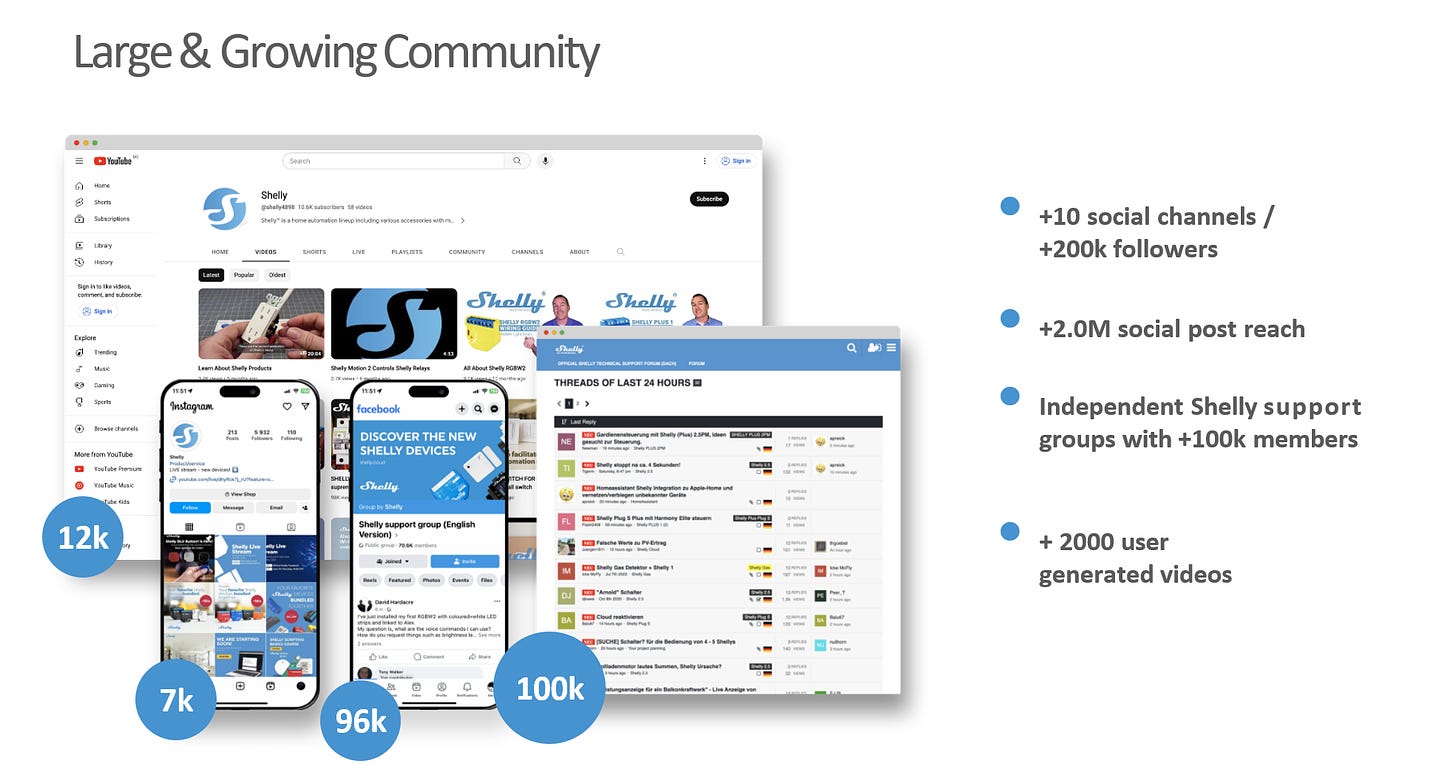

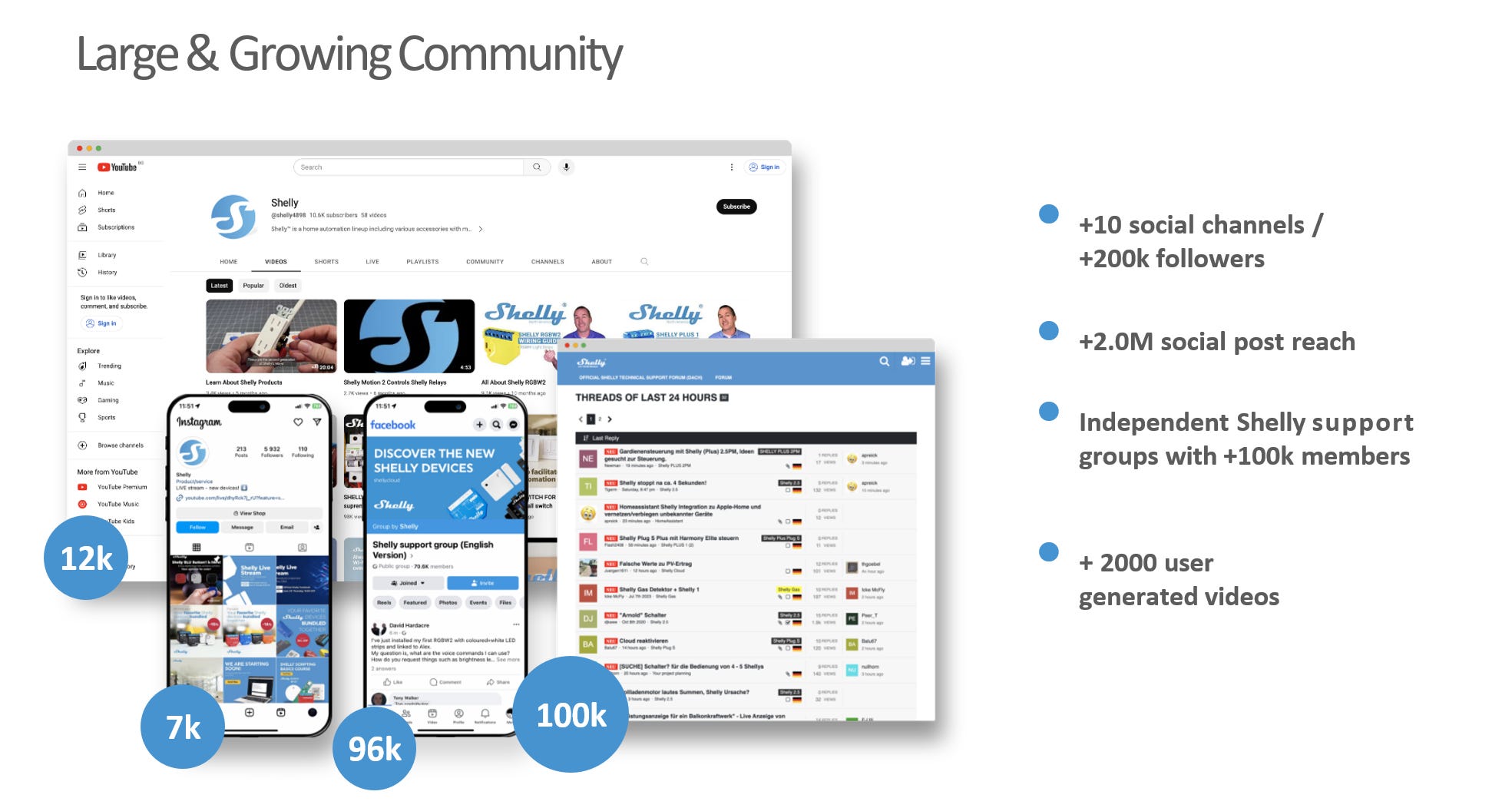

Big community with high engagement

Shelly Group has a huge online community. YouTube channels and Facebook groups alone provide free marketing for Shelly, which brings millions in revenue. These communities are where customers share tips and tricks, experiences with the products, and even suggestions to the management, which usually get replied to by the company.

So far, this has been their main driver of growth. The fact that Facebook communities and YouTube videos built this multi-million dollar company alone shows how much the consumers love the product.

European brand

Most customers could probably find Asian products in the same price range as Shelly’s. That said, the company positions itself as a European brand with higher quality and standards. Even the cloud service is completely based in Germany.

If Shelly is good enough for Audi, it is good enough for most people

Risks/weaknesses

Manufacturing in China

If Europe's relationship with China deteriorates further, there is a risk that their manufacturing could be disrupted or margins reduced. This would only be a short-term problem, though, as I mentioned, there is a plan built for this scenario.

Liquidity

Management has discussed this extensively and tried to solve it by listing Shelly on XETRA, but that is only one piece of the puzzle. Low liquidity can cause huge swings, and investors must be ready to deal with them. Shelly Group has already risen 44% YTD and could definitely come down a bit like Kinsale did. I’m sure it will outperform in the long term but don't get in if you want to buy and hold for 6-12 months.

Competition

Let's agree that smart home devices are not the most unique product. Even though Shelly Group stands out from the crowd, it is still possible that with the market becoming more attractive, competitors could spring up and reduce Shelly's growth.

Valuation

As with every single high-growing small cap, the valuation is an important part, but not THE most important one.

Growth

Management has guided that they are striving to achieve >200M revenue and >50M EBIT in 2026. This would represent a CAGR of 40%+, and you have to remember that they set their internal rates even higher.

Past growth:

5Yr EPS growth: 54.68%

5Yr revenue growth: 26.7%

Their current valuation:

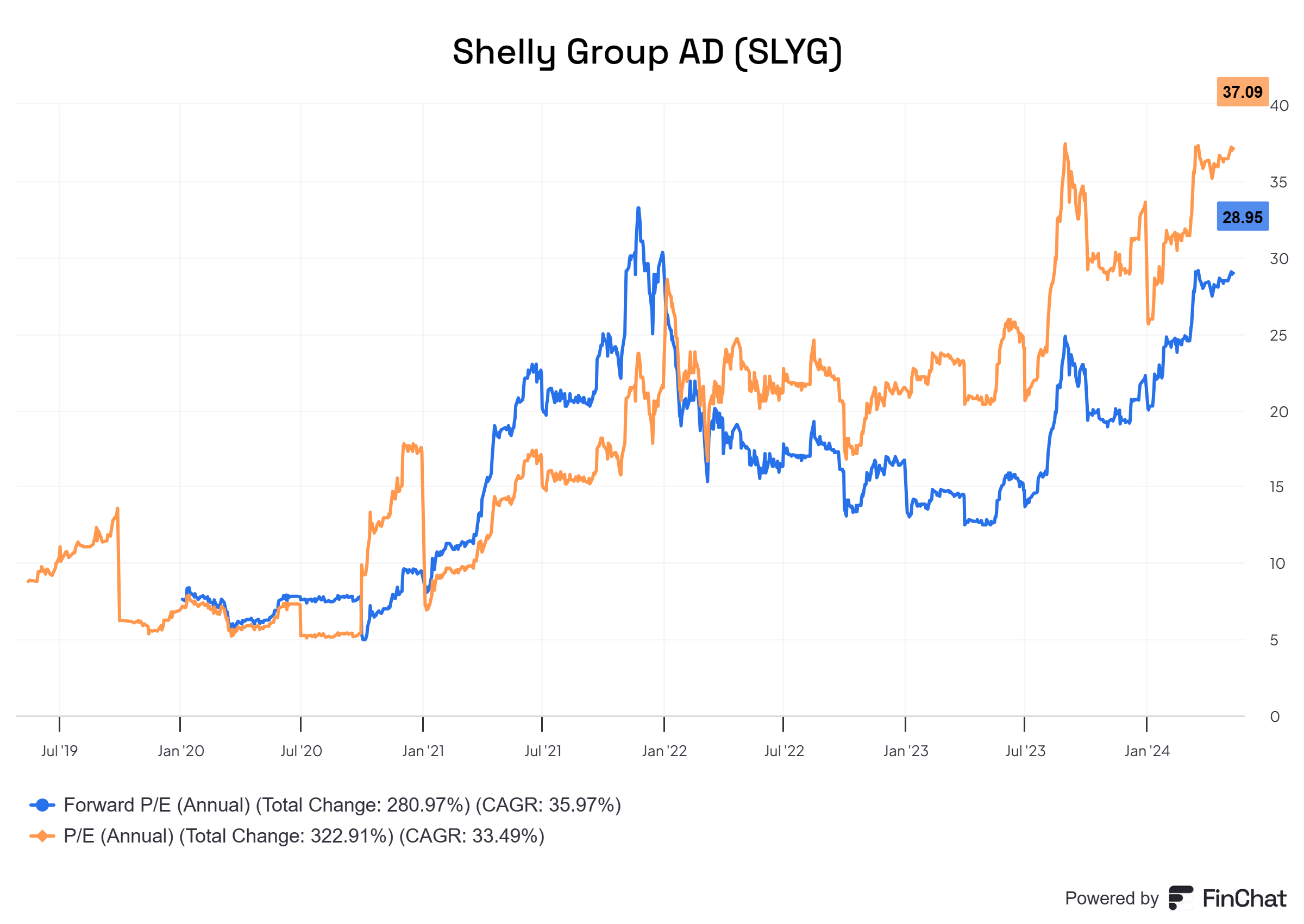

Trailing P/E: 37

Forward P/E: 29

PEG: 1.2-1.4

Overall, Shelly Group is not the cheapest company out there, but its projected growth, opportunities, and strengths make up for it.

Nevertheless, in companies like this, I'm sure there could be an opening to buy at a more attractive price, so I would suggest you get some shares now, but be prepared to buy 15-25% lower. I definitely will.

Calling my shot

In the next 3 years, assuming that Russia invading Europe is not a scenario, I believe Shelly's stock price will compound at 25-30% annually and then slow down to 15-20% annual returns. This is more than enough for me personally to justify a position.

Summary

In conclusion, Shelly Group is a high-grower emerging company that will continue to benefit from modernization, climate laws, and the increasing demand for easier home controls. The company could grow significantly from further European expansion and a potential yet difficult one in the USA. One thing I don’t love is the valuation. Even though high growth is predicted, volatile periods are always a possibility in low-float emerging stocks, especially in highly valued ones, so you have to account for that when deciding the size of the position. Nevertheless, one thing is clear - the management is more than capable of leading this great business, and I would not trust anyone else to do it.

Great read!

Great research - I am actually meeting with the management team Monday. Perhaps we can compare notes after.